7 Uncertainty

Prerequisites

We will use these package in this chapter:

library("tidyverse")

library("forcats")

library("lubridate")

library("stringr")

library("modelr")

library("broom")

library("purrr")7.1 Estimation

7.1.1 Unbiasedness and Consistency

In these simulations, we draw a sample of size n from normal distributions with means mu0 and mu1 and standard deviations sd0 and sd1 respectively,

n <- 100

mu0 <- 0

sd0 <- 1

mu1 <- 1

sd1 <- 1

smpl <- tibble(id = seq_len(n),

# Y if not treated

Y0 = rnorm(n, mean = mu0, sd = sd0),

# Y if treated

Y1 = rnorm(n, mean = mu1, sd = sd1),

# individual treatment effects

tau = Y1 - Y0)The SATE is:

SATE <- mean(smpl[["tau"]])

SATE

#> [1] 0.952Simulations of RCTs. Write a function that takes the sample as an input smpl, then randomly assigns the treatment to each individual:

sim_treat <- function(smpl) {

n <- nrow(smpl)

SATE <- mean(smpl[["tau"]])

# indexes of obs receiving treatment

idx <- sample(seq_len(n), floor(nrow(smpl) / 2), replace = FALSE)

# treat variable are those receiving treatment, else 0

smpl[["treat"]] <- as.integer(seq_len(nrow(smpl)) %in% idx)

smpl %>%

mutate(Y_obs = if_else(treat == 1L, Y1, Y0)) %>%

group_by(treat) %>%

summarise(Y_obs = mean(Y_obs)) %>%

spread(treat, Y_obs) %>%

rename(Y1_mean = `1`, Y0_mean = `0`) %>%

mutate(diff_mean = Y1_mean - Y0_mean,

est_error = diff_mean - SATE)

}This returns a data frame with columns: Y0_mean (mean \(Y\) for observations not receiving the treatment), Y1_mean (mean \(Y\) for observations receiving the treatment), diff (difference in mean values between the two groups), and est_error (difference between the estimated difference and the known SATE):

sim_treat(smpl)

#> # A tibble: 1 x 4

#> Y0_mean Y1_mean diff_mean est_error

#> <dbl> <dbl> <dbl> <dbl>

#> 1 -0.0570 0.875 0.932 -0.0207Rerun this function sims times:

sims <- 5000

sate_sims <- map_df(seq_len(sims), ~ sim_treat(smpl))

summary(sate_sims[["est_error"]])

#> Min. 1st Qu. Median Mean 3rd Qu. Max.

#> -0.484 -0.087 -0.002 -0.001 0.085 0.414Simulate the PATE:

PATE <- mu1 - mu0sim_pate <- function(n, mu0, mu1, sd0, sd1) {

smpl <- tibble(Y0 = rnorm(n, mean = mu0, sd = sd0),

Y1 = rnorm(n, mean = mu1, sd = sd1),

tau = Y1 - Y0)

# indexes of obs receiving treatment

idx <- sample(seq_len(n), floor(nrow(smpl) / 2), replace = FALSE)

# treat variable are those receiving treatment, else 0

smpl[["treat"]] <- as.integer(seq_len(nrow(smpl)) %in% idx)

smpl %>%

mutate(Y_obs = if_else(treat == 1L, Y1, Y0)) %>%

group_by(treat) %>%

summarise(Y_obs = mean(Y_obs)) %>%

spread(treat, Y_obs) %>%

rename(Y1_mean = `1`, Y0_mean = `0`) %>%

mutate(diff_mean = Y1_mean - Y0_mean,

est_error = diff_mean - PATE)

}Example of one simulation

sim_pate(n, mu0, mu1, sd0, sd1)

#> # A tibble: 1 x 4

#> Y0_mean Y1_mean diff_mean est_error

#> <dbl> <dbl> <dbl> <dbl>

#> 1 -0.109 0.925 1.03 0.0338pate_sims <-

map_df(seq_len(sims), ~ sim_pate(n, mu0, mu1, sd0, sd1))

summary(pate_sims[["est_error"]])

#> Min. 1st Qu. Median Mean 3rd Qu. Max.

#> -0.677 -0.135 -0.004 -0.003 0.129 0.8537.1.2 Standard Error

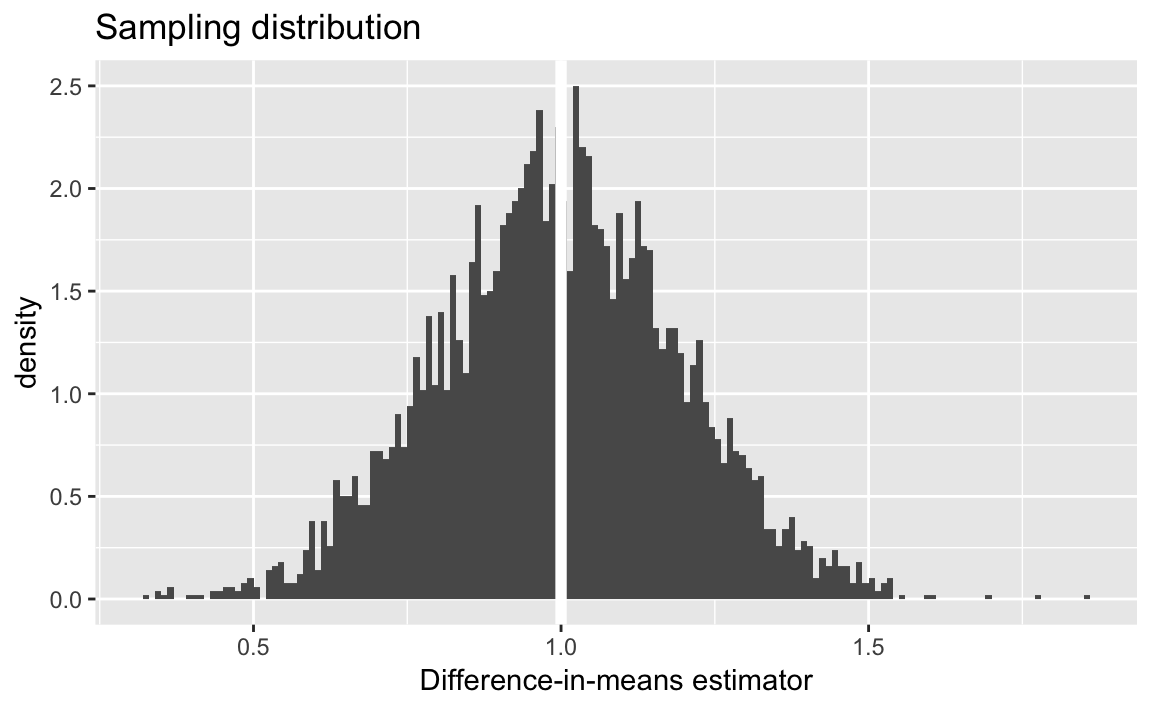

Plot of the sampling distribution of the difference-in-means estimator:

ggplot(pate_sims, aes(x = diff_mean, y = ..density..)) +

geom_histogram(binwidth = 0.01, boundary = 1) +

geom_vline(xintercept = PATE, colour = "white", size = 2) +

ggtitle("Sampling distribution") +

labs(x = "Difference-in-means estimator")

sd(pate_sims[["diff_mean"]])

#> [1] 0.196Simulate PATE with a standard error:

sim_pate_se <- function(n, mu0, mu1, sd0, sd1) {

# PATE - difference in means

PATE <- mu1 - mu0

# sample

smpl <- tibble(Y0 = rnorm(n, mean = mu0, sd = sd0),

Y1 = rnorm(n, mean = mu1, sd = sd1),

tau = Y1 - Y0)

# indexes of obs receiving treatment

idx <- sample(seq_len(n), floor(nrow(smpl) / 2), replace = FALSE)

# treat variable are those receiving treatment, else 0

smpl[["treat"]] <- as.integer(seq_len(nrow(smpl)) %in% idx)

# sample

smpl %>%

mutate(Y_obs = if_else(treat == 1L, Y1, Y0)) %>%

group_by(treat) %>%

summarise(mean = mean(Y_obs),

var = var(Y_obs),

nobs = n()) %>%

summarise(diff_mean = diff(mean),

se = sqrt(sum(var / nobs)),

est_error = diff_mean - PATE)

}Run a single simulation:

sim_pate_se(n, mu0, mu1, sd0, sd1)

#> # A tibble: 1 x 3

#> diff_mean se est_error

#> <dbl> <dbl> <dbl>

#> 1 1.05 0.190 0.0539Run sims simulations:

sims <- 5000

pate_sims_se <-

map_df(seq_len(sims), ~ sim_pate_se(n, mu0, mu1, sd0, sd1))Standard deviation of difference-in-means

sd(pate_sims_se[["diff_mean"]])

#> [1] 0.199Mean of standard errors,

mean(pate_sims_se[["se"]])

#> [1] 0.27.1.3 Confidence Intervals

Calculate a \(p\%\) confidence interval for the binomial distribution:

# Sample size

n <- 1000

# point estimate

x_bar <- 0.6

# standard error

se <- sqrt(x_bar * (1 - x_bar) / n)

# Desired Confidence levels

levels <- c(0.99, 0.95, 0.90)tibble(level = levels) %>%

mutate(

ci_lower = x_bar - qnorm(1 - (1 - level) / 2) * se,

ci_upper = x_bar + qnorm(1 - (1 - level) / 2) * se

)

#> # A tibble: 3 x 3

#> level ci_lower ci_upper

#> <dbl> <dbl> <dbl>

#> 1 0.99 0.560 0.640

#> 2 0.95 0.570 0.630

#> 3 0.9 0.575 0.625Calculate the coverage ratio of the 95% confidence interval in the PATE simulations.

level <- 0.95

pate_sims_se %>%

mutate(ci_lower = diff_mean - qnorm(1 - (1 - level) / 2) * se,

ci_upper = diff_mean + qnorm(1 - (1 - level) / 2) * se,

includes_pate = PATE > ci_lower & PATE < ci_upper) %>%

summarise(coverage = mean(includes_pate))

#> # A tibble: 1 x 1

#> coverage

#> <dbl>

#> 1 0.948To do this for multiple levels encapsulate the above code in a function with arguments .data (the data frame) and the confidence level, level:

pate_sims_coverage <- function(.data, level = 0.95) {

mutate(.data,

ci_lower = diff_mean - qnorm(1 - (1 - level) / 2) * se,

ci_upper = diff_mean + qnorm(1 - (1 - level) / 2) * se,

includes_pate = PATE > ci_lower & PATE < ci_upper) %>%

summarise(coverage = mean(includes_pate))

}

pate_sims_coverage(pate_sims_se, 0.95)

#> # A tibble: 1 x 1

#> coverage

#> <dbl>

#> 1 0.948

pate_sims_coverage(pate_sims_se, 0.99)

#> # A tibble: 1 x 1

#> coverage

#> <dbl>

#> 1 0.989

pate_sims_coverage(pate_sims_se, 0.90)

#> # A tibble: 1 x 1

#> coverage

#> <dbl>

#> 1 0.898p <- 0.6

n <- 10

alpha <- 0.05

sims <- 5000Define a function that samples from a Bernoulli distribution, calculates its standard error, and returns a logical value as to whether it contains the true value:

binom_ci_contains <- function(n, p, alpha = 0.05) {

x <- rbinom(n, size = 1, prob = p)

x_bar <- mean(x)

se <- sqrt(x_bar * (1 - x_bar) / n)

ci_lower <- x_bar - qnorm(1 - alpha / 2) * se

ci_upper <- x_bar + qnorm(1 - alpha / 2) * se

(ci_lower <= p) & (p <= ci_upper)

}We can run this once for given sample size:

n <- 10

binom_ci_contains(n, p)

#> [1] FALSEUsing map_df we can rerun it sims times and calculate the coverage proportion:

mean(map_lgl(seq_len(sims), ~ binom_ci_contains(n, p)))

#> [1] 0.905Encapsulate the above code in a function that calculates the coverage of a confidence interval with size, n, and success probability, p:

binom_ci_coverage <- function(n, p, sims) {

mean(map_lgl(seq_len(sims), ~ binom_ci_contains(n, p)))

}Use binom_ci_coverage to calculate CI coverage for multiple values of the sample size:

tibble(n = c(10L, 100L, 1000L)) %>%

mutate(coverage = map_dbl(n, binom_ci_coverage, p = !!p, sims = !!sims))

#> # A tibble: 3 x 2

#> n coverage

#> <int> <dbl>

#> 1 10 0.900

#> 2 100 0.943

#> 3 1000 0.9487.1.4 Margin of Error and Sample Size Calculation in Polls

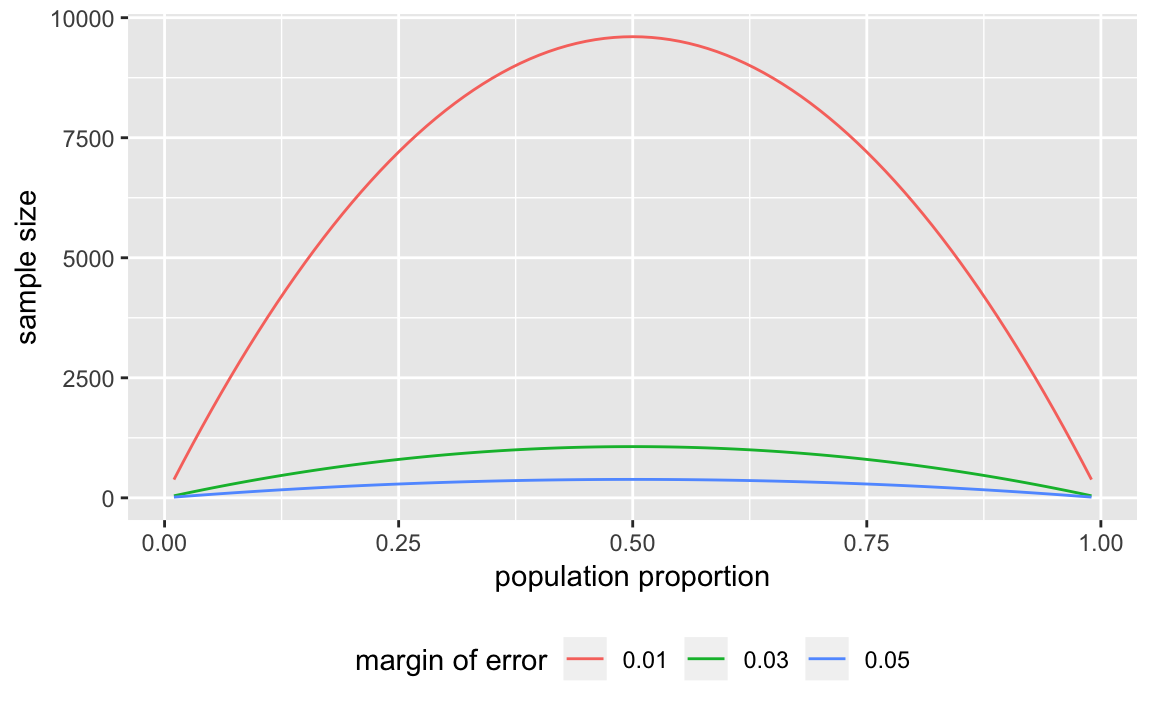

Write a function to calculate the sample size needed for a given proportion.

moe_pop_prop <- function(MoE) {

tibble(p = seq(from = 0.01, to = 0.99, by = 0.01),

n = 1.96 ^ 2 * p * (1 - p) / MoE ^ 2,

MoE = MoE)

}

moe_pop_prop(0.01)

#> # A tibble: 99 x 3

#> p n MoE

#> <dbl> <dbl> <dbl>

#> 1 0.01 380. 0.01

#> 2 0.02 753. 0.01

#> 3 0.03 1118. 0.01

#> 4 0.04 1475. 0.01

#> 5 0.05 1825. 0.01

#> 6 0.06 2167. 0.01

#> # ... with 93 more rowsThen use map_df to call this function for different margins of error, and return the entire thing as a data frame with columns: n, p, and MoE.

MoE <- c(0.01, 0.03, 0.05)

props <- map_df(MoE, moe_pop_prop)Since its a data frame, its easy to plot with ggplot:

ggplot(props, aes(x = p, y = n, colour = factor(MoE))) +

geom_line() +

labs(colour = "margin of error",

x = "population proportion",

y = "sample size") +

theme(legend.position = "bottom") read_csv already recognizes the date columns, so we don’t need to convert them. The 2008 election was on Nov 11, 2008, so we’ll store that in a variable.

read_csv already recognizes the date columns, so we don’t need to convert them. The 2008 election was on Nov 11, 2008, so we’ll store that in a variable.

ELECTION_DATE <- ymd(20081104)Load the final vote shares,

data("pres08", package = "qss")and polling data

data("polls08", package = "qss")We need to add an additional column to the polls08 data frame which contains the number of days until the election:

polls08 <- polls08 %>%

mutate(DaysToElection = as.integer(ELECTION_DATE - middate))For each state calculate the mean of the latest polls,

poll_pred <-

polls08 %>%

group_by(state) %>%

# latest polls in the state

filter(DaysToElection == min(DaysToElection)) %>%

# take mean of latest polls and convert from 0-100 to 0-1

summarise(Obama = mean(Obama) / 100)

# Add confidence itervals

# sample size

sample_size <- 1000

# confidence level

alpha <- 0.05

poll_pred <-

poll_pred %>%

mutate(se = sqrt(Obama * (1 - Obama) / sample_size),

ci_lwr = Obama + qnorm(alpha / 2) * se,

ci_upr = Obama + qnorm(1 - alpha / 2) * se)

# Add actual outcome

poll_pred <-

left_join(poll_pred,

select(pres08, state, actual = Obama),

by = "state") %>%

mutate(actual = actual / 100,

covers = (ci_lwr <= actual) & (actual <= ci_upr))

poll_pred

#> # A tibble: 51 x 7

#> state Obama se ci_lwr ci_upr actual covers

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <lgl>

#> 1 AK 0.39 0.0154 0.360 0.420 0.38 TRUE

#> 2 AL 0.36 0.0152 0.330 0.390 0.39 FALSE

#> 3 AR 0.44 0.0157 0.409 0.471 0.39 FALSE

#> 4 AZ 0.465 0.0158 0.434 0.496 0.45 TRUE

#> 5 CA 0.6 0.0155 0.570 0.630 0.61 TRUE

#> 6 CO 0.52 0.0158 0.489 0.551 0.54 TRUE

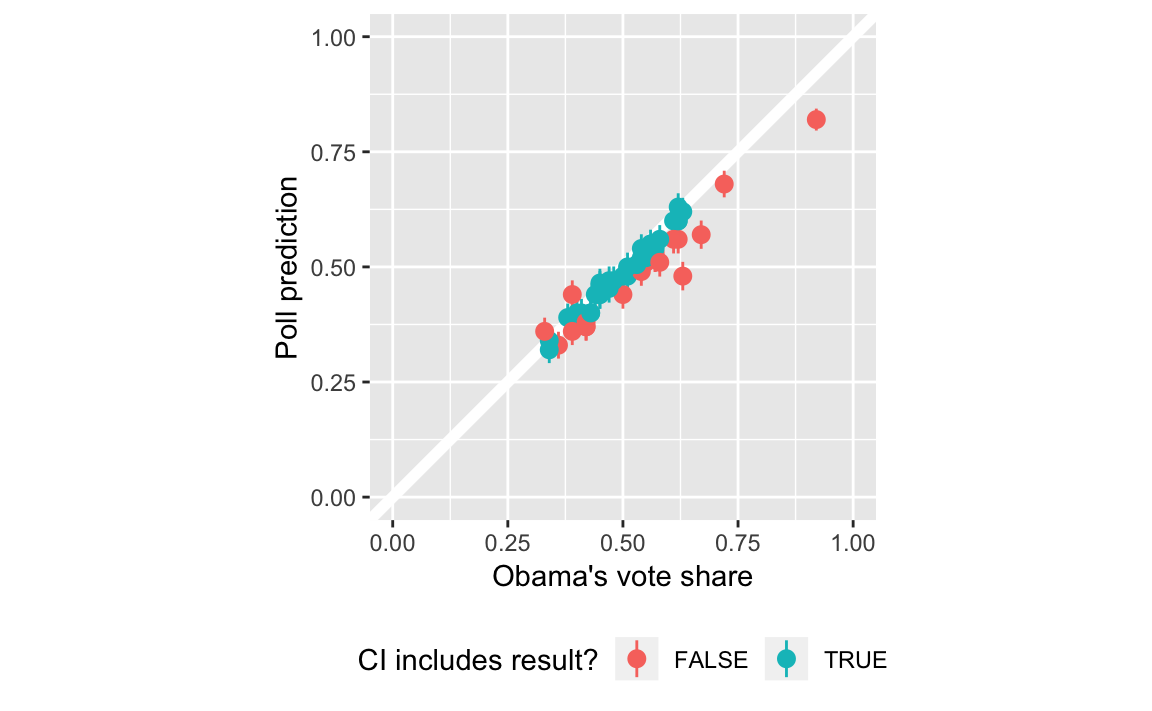

#> # ... with 45 more rowsIn the plot, color the point ranges by whether they include the election day outcome.

ggplot(poll_pred, aes(x = actual, y = Obama,

ymin = ci_lwr, ymax = ci_upr,

colour = covers)) +

geom_abline(intercept = 0, slope = 1, colour = "white", size = 2) +

geom_pointrange() +

scale_y_continuous("Poll prediction", limits = c(0, 1)) +

scale_x_continuous("Obama's vote share", limits = c(0, 1)) +

scale_colour_discrete("CI includes result?") +

coord_fixed() +

theme(legend.position = "bottom")

Proportion of polls with confidence intervals that include the election outcome?

poll_pred %>%

summarise(mean(covers))

#> # A tibble: 1 x 1

#> `mean(covers)`

#> <dbl>

#> 1 0.588poll_pred <-

poll_pred %>%

# calc bias

mutate(bias = Obama - actual) %>%

# bias corrected prediction, se, and CI

mutate(Obama_bc = Obama - mean(bias),

se_bc = sqrt(Obama_bc * (1 - Obama_bc) / sample_size),

ci_lwr_bc = Obama_bc + qnorm(alpha / 2) * se_bc,

ci_upr_bc = Obama_bc + qnorm(1 - alpha / 2) * se_bc,

covers_bc = (ci_lwr_bc <= actual) & (actual <= ci_upr_bc))

poll_pred %>%

summarise(mean(covers_bc))

#> # A tibble: 1 x 1

#> `mean(covers_bc)`

#> <dbl>

#> 1 0.7657.1.5 Analysis of Randomized Controlled Trials

Load the STAR data from the qss package,

data("STAR", package = "qss")Add meaningful labels to the classtype variable:

STAR <- STAR %>%

mutate(classtype = factor(classtype,

labels = c("small class", "regular class",

"regular class with aid")))Summarize scores by classroom type:

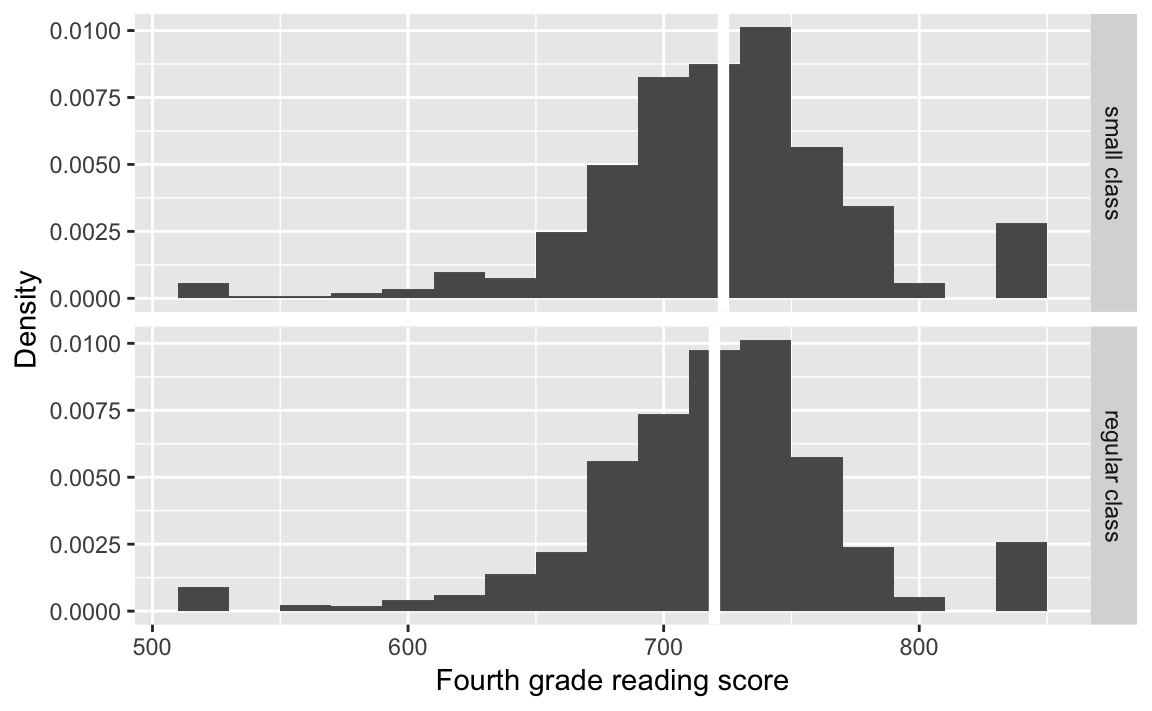

classtype_means <-

STAR %>%

group_by(classtype) %>%

summarise(g4reading = mean(g4reading, na.rm = TRUE))Plot the distribution of scores by classroom type:

classtypes_used <- c("small class", "regular class")

ggplot(filter(STAR,

classtype %in% classtypes_used,

!is.na(g4reading)),

aes(x = g4reading, y = ..density..)) +

geom_histogram(binwidth = 20) +

geom_vline(data = filter(classtype_means, classtype %in% classtypes_used),

mapping = aes(xintercept = g4reading),

colour = "white", size = 2) +

facet_grid(classtype ~ .) +

labs(x = "Fourth grade reading score", y = "Density")

alpha <- 0.05

star_estimates <-

STAR %>%

filter(!is.na(g4reading)) %>%

group_by(classtype) %>%

summarise(n = n(),

est = mean(g4reading),

se = sd(g4reading) / sqrt(n)) %>%

mutate(lwr = est + qnorm(alpha / 2) * se,

upr = est + qnorm(1 - alpha / 2) * se)

star_estimates

#> # A tibble: 3 x 6

#> classtype n est se lwr upr

#> <fct> <int> <dbl> <dbl> <dbl> <dbl>

#> 1 small class 726 723. 1.91 720. 727.

#> 2 regular class 836 720. 1.84 716. 723.

#> 3 regular class with aid 791 721. 1.86 717. 724.

star_estimates %>%

filter(classtype %in% c("small class", "regular class")) %>%

# ensure that it is ordered small then regular

arrange(desc(classtype)) %>%

summarise(

se = sqrt(sum(se ^ 2)),

est = diff(est)

) %>%

mutate(ci_lwr = est + qnorm(alpha / 2) * se,

ci_up = est + qnorm(1 - alpha / 2) * se)

#> # A tibble: 1 x 4

#> se est ci_lwr ci_up

#> <dbl> <dbl> <dbl> <dbl>

#> 1 2.65 3.50 -1.70 8.70

Use we could use spread and gather:

star_ate <-

star_estimates %>%

filter(classtype %in% c("small class", "regular class")) %>%

mutate(classtype = fct_recode(factor(classtype),

"small" = "small class",

"regular" = "regular class")) %>%

select(classtype, est, se) %>%

gather(stat, value, -classtype) %>%

unite(variable, stat, classtype) %>%

spread(variable, value) %>%

mutate(ate_est = est_small - est_regular,

ate_se = sqrt(se_small ^ 2 + se_regular ^ 2),

ci_lwr = ate_est + qnorm(alpha / 2) * ate_se,

ci_upr = ate_est + qnorm(1 - alpha / 2) * ate_se)

star_ate

#> # A tibble: 1 x 8

#> est_regular est_small se_regular se_small ate_est ate_se ci_lwr ci_upr

#> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 720. 723. 1.84 1.91 3.50 2.65 -1.70 8.707.1.6 Analysis Based on Student’s t-Distribution

Use filter to subset.

t.test(filter(STAR, classtype == "small class")$g4reading,

filter(STAR, classtype == "regular class")$g4reading)

#>

#> Welch Two Sample t-test

#>

#> data: filter(STAR, classtype == "small class")$g4reading and filter(STAR, classtype == "regular class")$g4reading

#> t = 1, df = 2000, p-value = 0.2

#> alternative hypothesis: true difference in means is not equal to 0

#> 95 percent confidence interval:

#> -1.70 8.71

#> sample estimates:

#> mean of x mean of y

#> 723 720The function t.test can also take a formula as its first parameter.

t.test(g4reading ~ classtype,

data = filter(STAR, classtype %in% c("small class", "regular class")))

#>

#> Welch Two Sample t-test

#>

#> data: g4reading by classtype

#> t = 1, df = 2000, p-value = 0.2

#> alternative hypothesis: true difference in means is not equal to 0

#> 95 percent confidence interval:

#> -1.70 8.71

#> sample estimates:

#> mean in group small class mean in group regular class

#> 723 7207.2 Hypothesis Testing

7.2.1 Tea-Testing Experiment

# Number of cups of tea

cups <- 4

# Number guessed correctly

k <- c(0, seq_len(cups))

true <- tibble(correct = k * 2,

n = choose(cups, k) * choose(cups, cups - k)) %>%

mutate(prob = n / sum(n))

true

#> # A tibble: 5 x 3

#> correct n prob

#> <dbl> <dbl> <dbl>

#> 1 0 1 0.0143

#> 2 2 16 0.229

#> 3 4 36 0.514

#> 4 6 16 0.229

#> 5 8 1 0.0143

sims <- 1000

guess <- tibble(guess = c("M", "T", "T", "M", "M", "T", "T", "M"))

randomize_tea <- function(df) {

# randomize the order of teas

assignment <- sample_frac(df, 1) %>%

rename(actual = guess)

bind_cols(df, assignment) %>%

summarise(correct = sum(guess == actual))

}

approx <-

map_df(seq_len(sims), ~ randomize_tea(guess)) %>%

count(correct) %>%

mutate(prob = n / sum(n))

left_join(select(approx, correct, prob_sim = prob),

select(true, correct, prob_exact = prob),

by = "correct") %>%

mutate(diff = prob_sim - prob_exact)

#> # A tibble: 5 x 4

#> correct prob_sim prob_exact diff

#> <dbl> <dbl> <dbl> <dbl>

#> 1 0 0.011 0.0143 -0.00329

#> 2 2 0.234 0.229 0.00543

#> 3 4 0.486 0.514 -0.0283

#> 4 6 0.253 0.229 0.0244

#> 5 8 0.016 0.0143 0.001717.2.2 The General Framework

The test functions like fisher.test do not work particularly well with data frames, and expect vectors or matrices as input, so tidyverse functions are less directly applicable

# all guesses correct

x <- tribble(~Guess, ~Truth, ~Number,

"Milk", "Milk", 4L,

"Milk", "Tea", 0L,

"Tea", "Milk", 0L,

"Tea", "Tea", 4L)

x

#> # A tibble: 4 x 3

#> Guess Truth Number

#> <chr> <chr> <int>

#> 1 Milk Milk 4

#> 2 Milk Tea 0

#> 3 Tea Milk 0

#> 4 Tea Tea 4

# 6 correct guesses

y <- x %>%

mutate(Number = c(3L, 1L, 1L, 3L))

y

#> # A tibble: 4 x 3

#> Guess Truth Number

#> <chr> <chr> <int>

#> 1 Milk Milk 3

#> 2 Milk Tea 1

#> 3 Tea Milk 1

#> 4 Tea Tea 3

# Turn into a 2x2 table for fisher.test

select(spread(x, Truth, Number), -Guess)

#> # A tibble: 2 x 2

#> Milk Tea

#> <int> <int>

#> 1 4 0

#> 2 0 4

# Use spread to make it a 2 x 2 table

fisher.test(select(spread(x, Truth, Number), -Guess),

alternative = "greater")

#>

#> Fisher's Exact Test for Count Data

#>

#> data: select(spread(x, Truth, Number), -Guess)

#> p-value = 0.01

#> alternative hypothesis: true odds ratio is greater than 1

#> 95 percent confidence interval:

#> 2 Inf

#> sample estimates:

#> odds ratio

#> Inf

fisher.test(select(spread(y, Truth, Number), -Guess))

#>

#> Fisher's Exact Test for Count Data

#>

#> data: select(spread(y, Truth, Number), -Guess)

#> p-value = 0.5

#> alternative hypothesis: true odds ratio is not equal to 1

#> 95 percent confidence interval:

#> 0.212 621.934

#> sample estimates:

#> odds ratio

#> 6.417.2.3 One-Sample Tests

n <- 1018

x_bar <- 550 / n

se <- sqrt(0.5 * 0.5 / n) # standard deviation of sampling distribution

# upper red area in the figure

upper <- pnorm(x_bar, mean = 0.5, sd = se, lower.tail = FALSE)

# lower red area in the figure; identical to the upper area

lower <- pnorm(0.5 - (x_bar - 0.5), mean = 0.5, sd = se)

# two side p value

upper + lower

#> [1] 0.0102

2 * upper

#> [1] 0.0102

# one sided p value

upper

#> [1] 0.00508

z_score <- (x_bar - 0.5) / se

z_score

#> [1] 2.57

pnorm(z_score, lower.tail = FALSE) # one-sided p-value

#> [1] 0.00508

2 * pnorm(z_score, lower.tail = FALSE) # two-sided p-value

#> [1] 0.0102

# 99% confidence interval contains 0.5

c(x_bar - qnorm(0.995) * se, x_bar + qnorm(0.995) * se)

#> [1] 0.500 0.581

# 95% confidence interval does not contain 0.5

c(x_bar - qnorm(0.975) * se, x_bar + qnorm(0.975) * se)

#> [1] 0.510 0.571

# no continuity correction to get the same p-value as above

prop.test(550, n = n, p = 0.5, correct = FALSE)

#>

#> 1-sample proportions test without continuity correction

#>

#> data: 550 out of n, null probability 0.5

#> X-squared = 7, df = 1, p-value = 0.01

#> alternative hypothesis: true p is not equal to 0.5

#> 95 percent confidence interval:

#> 0.510 0.571

#> sample estimates:

#> p

#> 0.54

# with continuity correction

prop.test(550, n = n, p = 0.5)

#>

#> 1-sample proportions test with continuity correction

#>

#> data: 550 out of n, null probability 0.5

#> X-squared = 6, df = 1, p-value = 0.01

#> alternative hypothesis: true p is not equal to 0.5

#> 95 percent confidence interval:

#> 0.509 0.571

#> sample estimates:

#> p

#> 0.54

prop.test(550, n = n, p = 0.5, conf.level = 0.99)

#>

#> 1-sample proportions test with continuity correction

#>

#> data: 550 out of n, null probability 0.5

#> X-squared = 6, df = 1, p-value = 0.01

#> alternative hypothesis: true p is not equal to 0.5

#> 99 percent confidence interval:

#> 0.499 0.581

#> sample estimates:

#> p

#> 0.54# two-sided one-sample t-test

t.test(STAR$g4reading, mu = 710)

#>

#> One Sample t-test

#>

#> data: STAR$g4reading

#> t = 10, df = 2000, p-value <2e-16

#> alternative hypothesis: true mean is not equal to 710

#> 95 percent confidence interval:

#> 719 723

#> sample estimates:

#> mean of x

#> 7217.2.4 Two-sample tests

The ATE estimates are stored in a data frame, star_ate. Note that the dplyr function transmute is like mutate, but only returns the variables specified in the function.

star_ate %>%

transmute(p_value_1sided = pnorm(-abs(ate_est),

mean = 0, sd = ate_se),

p_value_2sided = 2 * pnorm(-abs(ate_est), mean = 0,

sd = ate_se))

#> # A tibble: 1 x 2

#> p_value_1sided p_value_2sided

#> <dbl> <dbl>

#> 1 0.0935 0.187

t.test(g4reading ~ classtype,

data = filter(STAR, classtype %in% c("small class", "regular class")))

#>

#> Welch Two Sample t-test

#>

#> data: g4reading by classtype

#> t = 1, df = 2000, p-value = 0.2

#> alternative hypothesis: true difference in means is not equal to 0

#> 95 percent confidence interval:

#> -1.70 8.71

#> sample estimates:

#> mean in group small class mean in group regular class

#> 723 720or

t.test(filter(STAR, classtype == "small class")$g4reading,

filter(STAR, classtype == "regular class")$g4reading)

#>

#> Welch Two Sample t-test

#>

#> data: filter(STAR, classtype == "small class")$g4reading and filter(STAR, classtype == "regular class")$g4reading

#> t = 1, df = 2000, p-value = 0.2

#> alternative hypothesis: true difference in means is not equal to 0

#> 95 percent confidence interval:

#> -1.70 8.71

#> sample estimates:

#> mean of x mean of y

#> 723 720data("resume", package = "qss")

x <- resume %>%

count(race, call) %>%

spread(call, n) %>%

ungroup()

x

#> # A tibble: 2 x 3

#> race `0` `1`

#> <chr> <int> <int>

#> 1 black 2278 157

#> 2 white 2200 235

prop.test(as.matrix(select(x, -race)), alternative = "greater")

#>

#> 2-sample test for equality of proportions with continuity

#> correction

#>

#> data: as.matrix(select(x, -race))

#> X-squared = 20, df = 1, p-value = 2e-05

#> alternative hypothesis: greater

#> 95 percent confidence interval:

#> 0.0188 1.0000

#> sample estimates:

#> prop 1 prop 2

#> 0.936 0.903Assign sample sizes and proportions, then calculate point estimates, standard error, z-statistic and one-sided p-value.

n0 <- sum(resume$race == "black")

n1 <- sum(resume$race == "white")

p <- mean(resume$call)

p0 <- mean(filter(resume, race == "black")$call)

p1 <- mean(filter(resume, race == "white")$call)

est <- p1 - p0

est

#> [1] 0.032

se <- sqrt(p * (1 - p) * (1 / n0 + 1 / n1))

se

#> [1] 0.0078

zstat <- est / se

zstat

#> [1] 4.11

pnorm(-abs(zstat))

#> [1] 1.99e-05The only thing that changed is using filter for selecting the groups.

7.2.5 Power Analysis

Set the parameters: the sample size,

n <- 250the population proportional under the alternative data generating process,

p_star <- 0.48the null hypothesis,

p <- 0.5the p-value,

alpha <- 0.05and

cr_value <- qnorm(1 - alpha / 2)The standard errors under the hypothetical data generating process is

se_star <- sqrt(p_star * (1 - p_star) / n)and the standard error under the null is

se <- sqrt(p * (1 - p) / n)The power for this test is

pnorm(p - cr_value * se, mean = p_star, sd = se_star) +

pnorm(p + cr_value * se, mean = p_star, sd = se_star,

lower.tail = FALSE)

#> [1] 0.0967The parameters (sample sizes and proportions) are

n1 <- 500

n0 <- 500

p1_star <- 0.05

p0_star <- 0.1Calculate the overall call back rate as a weighted average,

p <- (n1 * p1_star + n0 * p0_star) / (n1 + n0)the standard error under the null,

se <- sqrt(p * (1 - p) * (1 / n1 + 1 / n0))the standard error under the hypothetical data generating process,

se.star <- sqrt(p1_star * (1 - p1_star) / n1 + p0_star * (1 - p0_star) / n0)pnorm(-cr_value * se, mean = p1_star - p0_star, sd = se.star) +

pnorm(cr_value * se, mean = p1_star - p0_star, sd = se.star,

lower.tail = FALSE)

#> [1] 0.852power.prop.test(n = 500, p1 = 0.05, p2 = 0.1, sig.level = 0.05)

#>

#> Two-sample comparison of proportions power calculation

#>

#> n = 500

#> p1 = 0.05

#> p2 = 0.1

#> sig.level = 0.05

#> power = 0.852

#> alternative = two.sided

#>

#> NOTE: n is number in *each* grouppower.prop.test(p1 = 0.05, p2 = 0.1, sig.level = 0.05, power = 0.9)

#>

#> Two-sample comparison of proportions power calculation

#>

#> n = 581

#> p1 = 0.05

#> p2 = 0.1

#> sig.level = 0.05

#> power = 0.9

#> alternative = two.sided

#>

#> NOTE: n is number in *each* grouppower.t.test(n = 100, delta = 0.25, sd = 1, type = "one.sample")

#>

#> One-sample t test power calculation

#>

#> n = 100

#> delta = 0.25

#> sd = 1

#> sig.level = 0.05

#> power = 0.697

#> alternative = two.sidedpower.t.test(power = 0.9, delta = 0.25, sd = 1, type = "one.sample")

#>

#> One-sample t test power calculation

#>

#> n = 170

#> delta = 0.25

#> sd = 1

#> sig.level = 0.05

#> power = 0.9

#> alternative = two.sidedpower.t.test(delta = 0.25, sd = 1, type = "two.sample",

alternative = "one.sided", power = 0.9)

#>

#> Two-sample t test power calculation

#>

#> n = 275

#> delta = 0.25

#> sd = 1

#> sig.level = 0.05

#> power = 0.9

#> alternative = one.sided

#>

#> NOTE: n is number in *each* group7.3 Linear Regression Model with Uncertainty

7.3.1 Linear Regression as a Generative Model

Load the minimum wage date included with the qss package:

data("minwage", package = "qss")minwage <- mutate(minwage,

fullPropBefore = fullBefore / (fullBefore + partBefore),

fullPropAfter = fullAfter / (fullAfter + partAfter),

NJ = as.integer(location == "PA"))fit_minwage <- lm(fullPropAfter ~ -1 + NJ + fullPropBefore +

wageBefore + chain, data = minwage)

fit_minwage

#>

#> Call:

#> lm(formula = fullPropAfter ~ -1 + NJ + fullPropBefore + wageBefore +

#> chain, data = minwage)

#>

#> Coefficients:

#> NJ fullPropBefore wageBefore chainburgerking

#> -0.0542 0.1688 0.0813 -0.0614

#> chainkfc chainroys chainwendys

#> -0.0966 -0.1522 -0.1659

fit_minwage1 <- lm(fullPropAfter ~ NJ + fullPropBefore +

wageBefore + chain, data = minwage)

fit_minwage1

#>

#> Call:

#> lm(formula = fullPropAfter ~ NJ + fullPropBefore + wageBefore +

#> chain, data = minwage)

#>

#> Coefficients:

#> (Intercept) NJ fullPropBefore wageBefore

#> -0.0614 -0.0542 0.1688 0.0813

#> chainkfc chainroys chainwendys

#> -0.0352 -0.0908 -0.1045

gather_predictions(slice(minwage, 1), fit_minwage, fit_minwage1) %>%

select(model, pred)

#> model pred

#> 1 fit_minwage 0.271

#> 2 fit_minwage1 0.2717.3.2 Inference about coefficients

Use the tidy function to return the coefficients, including confidence intervals, as a data frame:

data("women", package = "qss")

fit_women <- lm(water ~ reserved, data = women)

summary(fit_women)

#>

#> Call:

#> lm(formula = water ~ reserved, data = women)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -23.99 -14.74 -7.86 2.26 316.01

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 14.74 2.29 6.45 4.2e-10 ***

#> reserved 9.25 3.95 2.34 0.02 *

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 33.4 on 320 degrees of freedom

#> Multiple R-squared: 0.0169, Adjusted R-squared: 0.0138

#> F-statistic: 5.49 on 1 and 320 DF, p-value: 0.0197

tidy(fit_women)

#> term estimate std.error statistic p.value

#> 1 (Intercept) 14.74 2.29 6.45 4.22e-10

#> 2 reserved 9.25 3.95 2.34 1.97e-02You need to set conf.int = TRUE for tidy to include the confidence interval:

summary(fit_minwage)

#>

#> Call:

#> lm(formula = fullPropAfter ~ -1 + NJ + fullPropBefore + wageBefore +

#> chain, data = minwage)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.4862 -0.1813 -0.0281 0.1513 0.7509

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> NJ -0.0542 0.0332 -1.63 0.1034

#> fullPropBefore 0.1688 0.0566 2.98 0.0031 **

#> wageBefore 0.0813 0.0389 2.09 0.0374 *

#> chainburgerking -0.0614 0.1755 -0.35 0.7266

#> chainkfc -0.0966 0.1793 -0.54 0.5904

#> chainroys -0.1522 0.1832 -0.83 0.4066

#> chainwendys -0.1659 0.1853 -0.90 0.3711

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.244 on 351 degrees of freedom

#> Multiple R-squared: 0.635, Adjusted R-squared: 0.628

#> F-statistic: 87.2 on 7 and 351 DF, p-value: <2e-16

tidy(fit_minwage, conf.int = TRUE)

#> term estimate std.error statistic p.value conf.low conf.high

#> 1 NJ -0.0542 0.0332 -1.633 0.10343 -0.11953 0.0111

#> 2 fullPropBefore 0.1688 0.0566 2.981 0.00307 0.05744 0.2801

#> 3 wageBefore 0.0813 0.0389 2.090 0.03737 0.00478 0.1579

#> 4 chainburgerking -0.0614 0.1755 -0.350 0.72657 -0.40648 0.2837

#> 5 chainkfc -0.0966 0.1793 -0.539 0.59044 -0.44919 0.2560

#> 6 chainroys -0.1522 0.1832 -0.831 0.40664 -0.51238 0.2080

#> 7 chainwendys -0.1659 0.1853 -0.895 0.37115 -0.53031 0.19857.3.3 Inference about predictions

data("MPs", package = "qss")

MPs_labour <- filter(MPs, party == "labour")

MPs_tory <- filter(MPs, party == "tory")

labour_fit1 <- lm(ln.net ~ margin, data = filter(MPs_labour, margin < 0))

labour_fit2 <- lm(ln.net ~ margin, data = filter(MPs_labour, margin > 0))

tory_fit1 <- lm(ln.net ~ margin, data = filter(MPs_tory, margin < 0))

tory_fit2 <- lm(ln.net ~ margin, data = filter(MPs_tory, margin > 0))Predictions at the threshold. The broom function augment will return prediction fitted values and standard errors for each value, but not the confidence intervals themselves (we’d have to multiply the correct t-distribution with degrees of freedom.) So instead, we’ll directly use the predict function:

tory_y0 <-

predict(tory_fit1, interval = "confidence",

newdata = tibble(margin = 0)) %>% as_tibble()

tory_y0

#> # A tibble: 1 x 3

#> fit lwr upr

#> <dbl> <dbl> <dbl>

#> 1 12.5 12.1 13.0

tory_y1 <-

predict(tory_fit2, interval = "confidence",

newdata = tibble(margin = 0)) %>% as_tibble()

tory_y1

#> # A tibble: 1 x 3

#> fit lwr upr

#> <dbl> <dbl> <dbl>

#> 1 13.2 12.8 13.6Alternatively, using augment (and assuming a normal distribution since the number of observations is so large its not worth worrying about the t-distribution):

tory_y0 <-

augment(tory_fit1, newdata = tibble(margin = 0)) %>%

mutate(lwr = .fitted + qnorm(0.025) * .se.fit,

upr = .fitted + qnorm(0.975) * .se.fit)

tory_y0

#> margin .fitted .se.fit lwr upr

#> 1 0 12.5 0.214 12.1 13

tory_y1 <-

augment(tory_fit2, newdata = tibble(margin = 0)) %>%

mutate(lwr = .fitted + qnorm(0.025) * .se.fit,

upr = .fitted + qnorm(0.975) * .se.fit)

tory_y1

#> margin .fitted .se.fit lwr upr

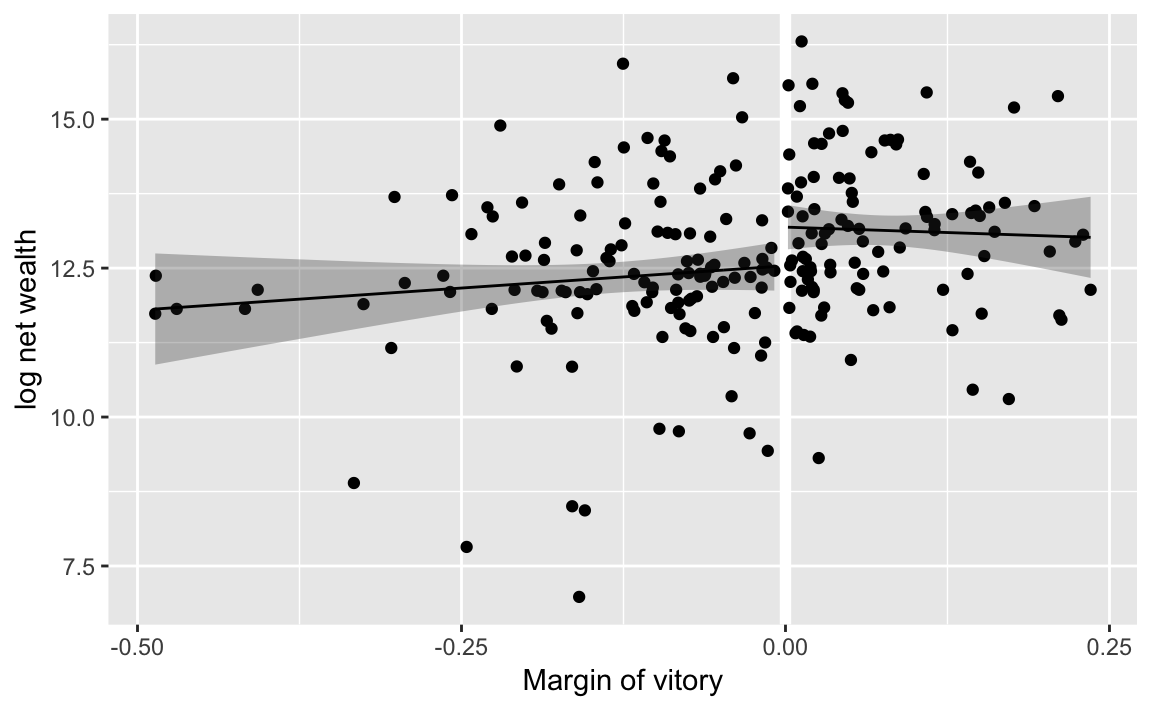

#> 1 0 13.2 0.192 12.8 13.6y1_range <- data_grid(filter(MPs_tory, margin <= 0), margin)

tory_y0 <- augment(tory_fit1, newdata = y1_range)

y2_range <- data_grid(filter(MPs_tory, margin >= 0), margin)

tory_y1 <- augment(tory_fit2, newdata = y2_range)ggplot() +

geom_ref_line(v = 0) +

geom_point(aes(y = ln.net, x = margin), data = MPs_tory) +

# plot losers

geom_ribbon(aes(x = margin,

ymin = .fitted + qnorm(0.025) * .se.fit,

ymax = .fitted + qnorm(0.975) * .se.fit),

data = tory_y0, alpha = 0.3) +

geom_line(aes(x = margin, y = .fitted), data = tory_y0) +

# plot winners

geom_ribbon(aes(x = margin,

ymin = .fitted + qnorm(0.025) * .se.fit,

ymax = .fitted + qnorm(0.975) * .se.fit),

data = tory_y1, alpha = 0.3) +

geom_line(aes(x = margin, y = .fitted), data = tory_y1) +

labs(x = "Margin of vitory", y = "log net wealth")

tory_y1 <- augment(tory_fit1, newdata = tibble(margin = 0))

tory_y1

#> margin .fitted .se.fit

#> 1 0 12.5 0.214

tory_y0 <- augment(tory_fit2, newdata = tibble(margin = 0))

tory_y0

#> margin .fitted .se.fit

#> 1 0 13.2 0.192

summary(tory_fit1)

#>

#> Call:

#> lm(formula = ln.net ~ margin, data = filter(MPs_tory, margin <

#> 0))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -5.320 -0.472 -0.035 0.663 3.580

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 12.538 0.214 58.54 <2e-16 ***

#> margin 1.491 1.291 1.15 0.25

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 1.43 on 119 degrees of freedom

#> Multiple R-squared: 0.0111, Adjusted R-squared: 0.00277

#> F-statistic: 1.33 on 1 and 119 DF, p-value: 0.251

summary(tory_fit2)

#>

#> Call:

#> lm(formula = ln.net ~ margin, data = filter(MPs_tory, margin >

#> 0))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -3.858 -0.877 0.001 0.830 3.126

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 13.188 0.192 68.69 <2e-16 ***

#> margin -0.728 1.982 -0.37 0.71

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 1.29 on 100 degrees of freedom

#> Multiple R-squared: 0.00135, Adjusted R-squared: -0.00864

#> F-statistic: 0.135 on 1 and 100 DF, p-value: 0.714Since we aren’t doing anything more with these values, there isn’t much benefit in keeping them in data frames.

# standard error

se_diff <- sqrt(tory_y0$.se.fit ^ 2 + tory_y1$.se.fit ^ 2)

se_diff

#> [1] 0.288

# point estimate

diff_est <- tory_y1$.fitted - tory_y0$.fitted

diff_est

#> [1] -0.65

# confidence interval

CI <- c(diff_est - se_diff * qnorm(0.975),

diff_est + se_diff * qnorm(0.975))

CI

#> [1] -1.2134 -0.0859

# hypothesis test

z_score <- diff_est / se_diff

# two sided p value

p_value <- 2 * pnorm(abs(z_score), lower.tail = FALSE)

p_value

#> [1] 0.0239